10 May 2019

The bitcoin bubble may have burst (though it’s predicted to be making a less splashy comebackthis year), but blockchain — the technology behind the cryptocurrency — is rapidly proliferating.

Earlier this year I gave a presentation to the Dallas Bar Association, where my co-presenter Ozz Siddiq and I discussed patent perspectives on quantum computing and blockchain technologies.

Ozz presented some very interesting developments in the world of blockchain patents. For example, large financial institutions like Bank of America are filing lots of patent applications in this field of technology.

So what does the blockchain patent landscape look like? First, here’s a quick summary of some basics of blockchain technology.

WHAT IS BLOCKCHAIN?

In very simple terms, a blockchain is a digital record of information that’s stored in a decentralized, public database. The data is linked across a large network of devices using cryptography, or software that secures the authenticity and integrity of the information.

Each “block” in the “chain” typically contains three specific pieces of data:

- Transactional data such as a timestamp and sale amount

- Encoded purchaser information in the form of a unique digital signature

- Unique “hash” code that inextricably links one block to another

HISTORY OF BLOCKCHAIN

Created in 2008, blockchain technology first came into play in the creation of the world’s most famous cryptocurrency, Bitcoin. And it soon became the foundation for many other cryptocurrencies, including LiteCoin, ZCash, and Ripple.

By 2014, however, it became clear that there were lots of ways to apply the decentralized, secure transaction-recording technology to support specific business models and uses.

BLOCKCHAIN APPLICATIONS

In 2015, Vitilak Buterin, who contributed to the coding and open source distribution of Bitcoin, built a second public blockchain called Ethereum. Aside from its cryptocurrency status, Ethereum has the ability to record a range of digital assets, including loans and contracts. These “smart contracts” can be processed automatically using a specified set of criteria.

Blockchain can also be thought of as a type of Distributed Ledger Technology (DLT). A distributed ledger can be used as a synchronized database for multiple sites in a network.

Blockchain and its related technologies have become more complex and new applications are being found every day. Here’s a brief overview of the technology’s historical patent trajectory.

OVERVIEW OF THE PATENT LANDSCAPE

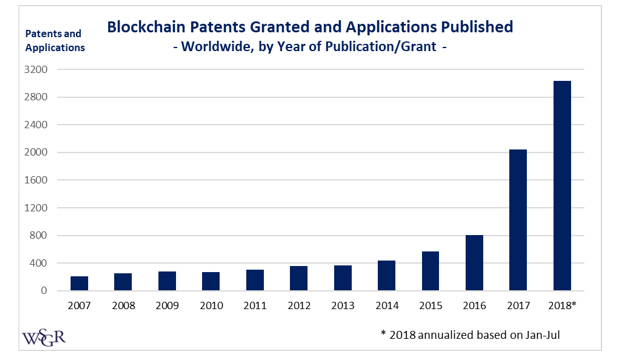

According to data compiled by the law firm Wilson Sonsini (WSGR — we’ve linked to their article on JDSUPRA), over 8,000 blockchain-related patents and patent applications have been filed worldwide, as of July 2018.

Blockchain patenting activity was pretty slow in the early years, only beginning to take off in 2015, with the creation of alternative blockchains like Ethereum. By 2016, it started to increase more rapidly, coinciding with Bitcoin’s historic mainstream rise in 2017.

TYPES OF BLOCKCHAIN PATENTS

Patent activity shows that commercial interest in the technology rose with the perceived profitability of Bitcoin investments. The WSGR data focuses on patents surrounding data processing and electrical computers — in line with fintech applications —and therefore highlights the bulk of patents in that industry. However, it’s worth noting that there are many other, less well-known classes of applications, including “surgery, amusement devices, cryptography and telecommunications.”

Geographic filing trends

WSGR reports that the top 5 jurisdictions for blockchain patent filings as of 2018 are:

- United States

- China

- Japan

- Europe

- South Korea

The US makes the top of the list by a wide margin, with over 1,300 patents and applications so far. China, while a strong second, hovers around 780 patents. Japan and Europe have 300 and 200 applications respectively, while South Korea sits at just over 150.

US AND INTERNATIONAL PATENTS

The US remains the top choice to file in, but the prevalence of filings outside the United States suggests that many companies foresee global commercial applications for blockchain technologies.

It’s safe to say that international flings are likely to play a key role in effective blockchain patent strategies, especially in the near future.

TOP PATENT ASSIGNEES (WORLDWIDE)

According to the research by WSGR, the top 5 patent assignees worldwide are:

- IBM

- Mastercard

- Sony

- Microsoft

- Panasonic/Matsushita

KEY TAKEAWAYS OF WORLDWIDE PATENT ASSIGNEES

IBM and Mastercard together account for almost 20% of all patents and applications held by the top 45 filers. Together, the top five patent filers account for almost 30% of the patents and applications held by the top 45 filers.

The top 12 filers, which also include Alibaba, Canon, Fujitsu, and Bank Of America, account for over 50% of the patents and applications held by the top 45 filers. A majority of worldwide patent filing can be attributed to a few key players, most of which are large corporations.

TOP PATENT ASSIGNEES (US)

The WSGR research shows that IBM clearly ranks first in US patent filings, with 190 applications and 61 patents. Microsoft holds second place with 25 applications and 30 patents and together with Bank Of America, Fujistsu, and Mastercard, make the Top 5. It’s worth noting that some companies on the “lower” end of the spectrum, such as Amazon (#8), have more patents than published applications (35 vs 8).

Overall, the top US assignees are relatively similar to top global assignees.

AVOID POTENTIAL PATENT PITFALLS

In the patent world, blockchain technology typically falls in the category of software-implemented inventions — and we’ve written extensively about the possible pitfalls with patenting software, especially in the wake of decisions like Alice.

The high turnout at our recent presentation on patent perspectives on blockchain technologies demonstrates the value of being informed about the potential pitfalls of blockchain patenting.

OVERCOMING 101 REJECTIONS

In navigating the patent process, knowing how to overcome common issues can mean the difference between a patent grant and a costly rejection.

A few tips to remember:

- In your patent application, be sure to discuss advantages and improvements over traditional technologies (e.g., databases). Emphasizing practical applications will help avoid subject matter eligibility rejections.

- Discuss how your blockchain-related invention improves the capability of the system as a whole. For example, can your invention be used to improve the operation of the blockchain itself?

- Don’t let the Examiner argue solely in the abstract. If your patent application is rejected, press the examiner to provide specific details to support the rejection.

- Don’t focus on results, but rather the structure of the system. While the advantages (e.g., speed, security, etc.) provided by your invention might be valuable, the features that produce those advantages will make the most compelling case for patentability.

A licensed patent attorney can help you navigate these issues. If you’ re developing blockchain technology and considering patent protection for your innovations, we’d love to hear from you!

Michael K. Henry, Ph.D.

Michael K. Henry, Ph.D., is a principal and the firm’s founding member. He specializes in creating comprehensive, growth-oriented IP strategies for early-stage tech companies.